Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

For many homeowners and aspiring buyers, mortgage interest rates can be a significant factor influencing their decision to move. As interest rates play a crucial role in determining the cost of homeownership, it’s natural to want to wait for more favorable rates before making a move.

On a weekly basis I talk to people who want to move, but express that the main thing holding them back is the 6-7% rates they’d have to pay. And this is totally understandable, especially for those who are currently locked in at a rate of 3% or less on our current home.

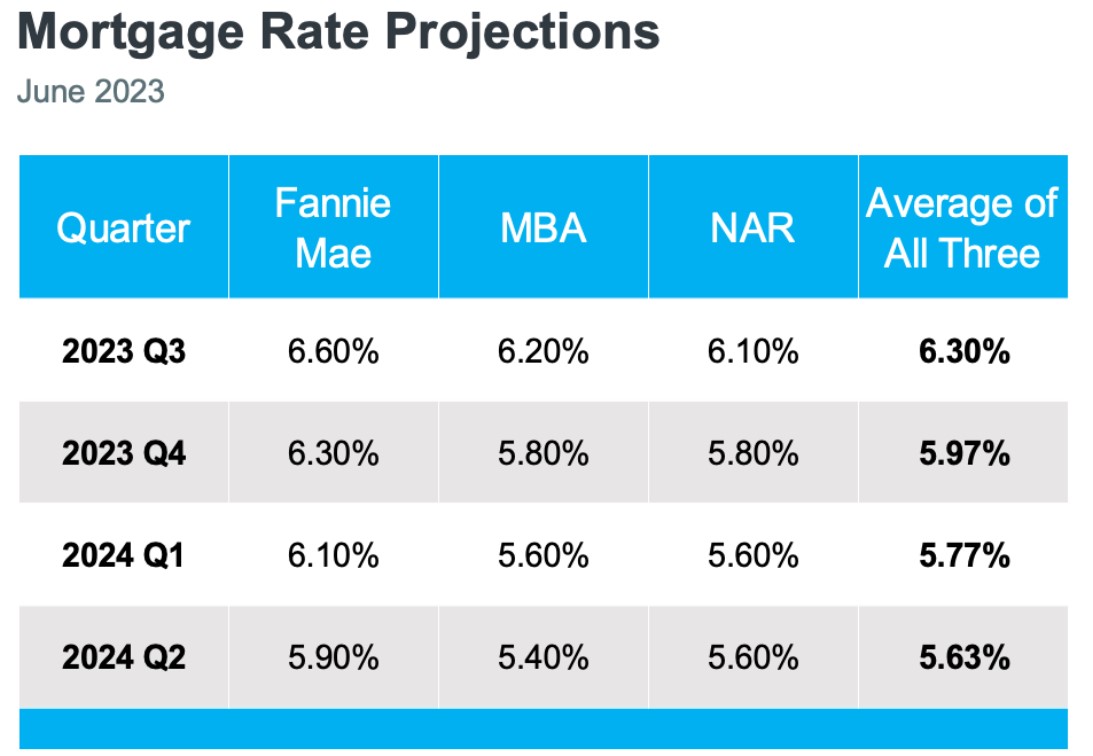

While notoriously difficult to forecast, below is a table from Keeping Current Matters that gives some direction as to where mortgage rates may be headed into the second quarter of 2024. As inflation is expected to cool, we have reason to be optimistic that mortgage rates will drop gradually as a response.

While the trend is positive, these projections are unlikely to do much to boost the confidence of potential homebuyers in the near term. And as a homeowner who enjoys a rate that is <3% right now, I get it.

But there are two perspectives I want to share for those whose hearts are set on making a move in the near future, but grappling with the current rates.

1. It’s important to look at rates historically

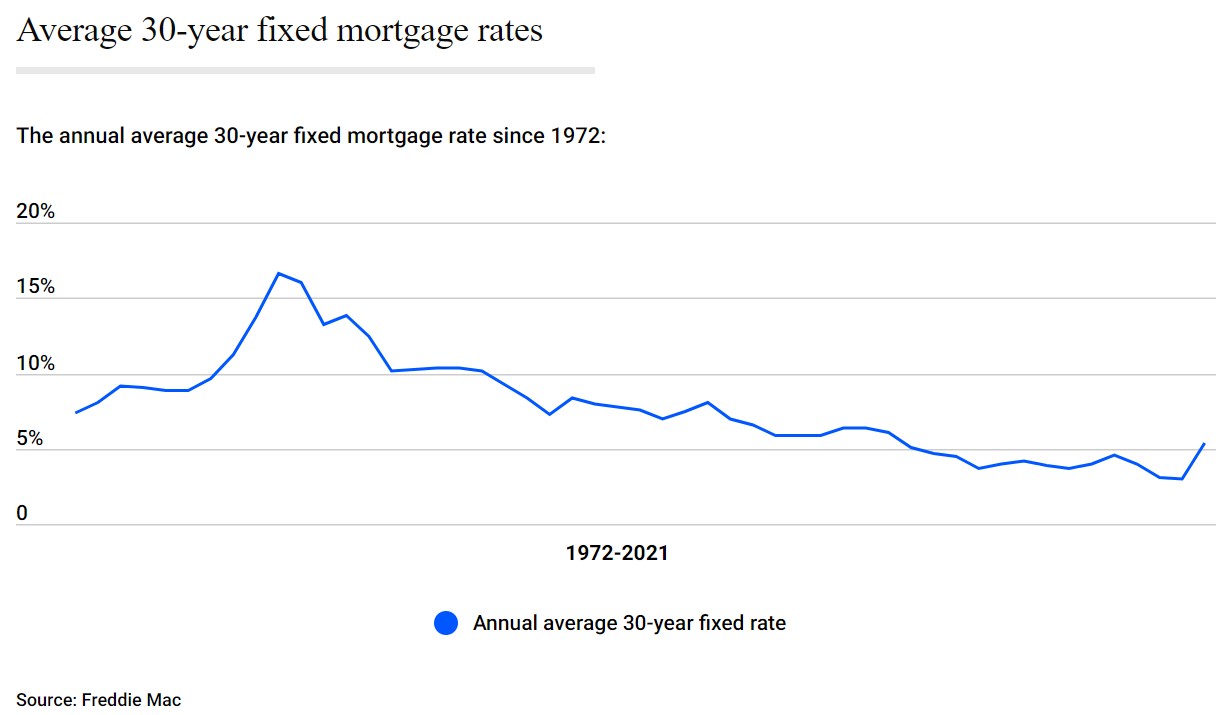

Consider that the average rate on a 30-year fixed loan over the past 50 years is approximately 7%, with a high of 16.63% in 1981 and a low of 2.96% in 2021.

This may not offer much comfort given the record low over the past 50 years is so recent. That said, it’s good to keep in mind that rates, just like home prices, fluctuate over time in response to myriad factors outside of our control.

2. Adjust to the new normal

Some experts doubt we will see mortgage rates below 3% again for a very long time; if ever. The “unicorn years” of 2020-2021 are behind us, and we may do well to accept the possibility that this era of real estate is truly an anomaly. (Furthermore, let’s hope we never see another global pandemic like COVID-19 in our lifetime, or our childrens’ lifetime!).

You may have heard the phrase, “marry the home, date the rate.” If you find a home you love and can afford the monthly PITI (principal, interest, tax, insurance) payment amount, you can always refinance down the road when rates drop.